La Rosa Holdings Makes 10th Acquisition; Reaffirms Target of $100 Million 2024 Exit Run Rate ($LRHC)

")

La Rosa Holdings Corp. (NASDAQ: LRHC) is on a torrid pace to become a much larger company. Last month, supporting that thesis, LRHC announced acquiring 51% of franchisee Prestige, making it the tenth acquisition since its public listing last year. Like its others, this one is also a top-performing office, evidenced by its generating 2023 revenues of $4.7 and, more importantly, from an investor perspective, positive net income.

More than a financial boost, the deal also strengthened La Rosa’s market position in Polk County, Florida, by enabling it to leverage its 51% interest to capitalize on the selling strength of Prestige’s 162 agents. Size-wise, Prestige is the second-largest brokerage in terms of agent count and the third-largest in real estate sales within Polk County for 2023.

That could expedite La Rosa reaching its goal of an annualized revenue run rate of $100 million by the end of this year. Better still, the accretive nature of the transaction to its other nine put bottom-line EPS in the crosshairs, potentially as early as the first half of 2025. Remember, though, La Rosa is still in its early growth innings. The string of acquisitions is expected to continue, especially with CEO Joe La Rosa in front, emphasizing his strategy to roll up profitable offices, consolidate market presence, and benefit from economies of scale that result from seamlessly integrating newly acquired assets with current portfolio assets.

The better news is that despite its microcap size, La Rosa is showing it can more than compete with the larger sector players; its operational performance can be more impressive. And that’s simultaneous to the costs involved in acquiring new assets.

Being Nimble Has Its Advantages

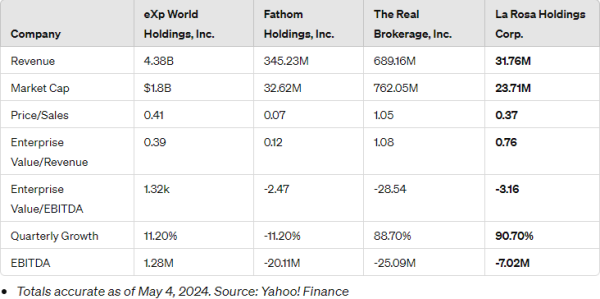

Compared to eXp World Holdings (NASDAQ: EXPI), The Real Brokerage (NASDAQ: REAX), and Fathom Holdings (NASDAQ: FTHM), La Rosa proves that being aggressive but nimble in practice can return quick, more efficient ROI for itself and its stakeholders. For instance, although La Rosa’s market cap is smaller than the other three listed companies, that’s okay. In this case, it exposes a disconnect, not based on dollar-for-dollar comparisons but from an asset portfolio that does not have the burden of carrying non- or underperforming assets. In other words, smart growth, especially accretive, can build tangible and manageable market cap increases by efficiently using available capital.

La Rosa’s financial efficiency, particularly evident in its Enterprise Value / Revenue ratio, is a strong indicator of its resource management. While REAX may have a higher ratio, La Rosa’s performance in other areas compensates. Its robust performance in this measure suggests that it’s generating more revenue relative to its enterprise value, a promising sign for potential growth. This efficiency can support a higher share price, a factor that influences the Price/Sales ratio.

La Rosa’s Price/Sales ratio handily beat FTHM’s and is on the heels of EXPI. While considerably below REAX, after factoring in additional acquisitions, this gap may close significantly. The current P/E for La Rosa exposes that its stock may be undervalued relative to its sales, especially with these numbers for all the comps as of the last reporting period. And here’s the value kicker—EV / EBITDA.

La Rosa may have negative EV / EBITDA ratios, but it’s important to note that they are significantly better than REAX and are nearly on par with FTHM, trailing by just a small margin. This strength isn’t by chance; it reflects La Rosa’s adept management of debt and operational expenses, setting it apart from its competitors. When considering efficiency, valuation, and growth potential, La Rosa stands out favorably among its more established counterparts. In fact, La Rosa has outperformed three out of four competitors in terms of EBITDA, with only EXPI surpassing it by posting earnings after its large sales volume. Meanwhile, REAX and FTHM lag far behind with substantial negative figures, highlighting La Rosa’s comparatively solid financial standing despite the challenges in the industry.

For growth stock investors, the Quarterly Growth performance is a crucial indicator. La Rosa’s impressive 90.7% increase not only tops the list but also sparks optimism. Outperforming EXPI, FTHM, and REAX, La Rosa’s growth is tangible and its potential is evident. Considering recent acquisitions that may not be factored into this analysis, La Rosa’s growth trajectory could be even more promising, igniting excitement for prospective investors.

While financial analysis is a key component of value assessment, it’s crucial to consider other factors that contribute to the La Rosa value proposition, particularly qualitative ones. These factors strengthen the already positive argument for its valuations to increase in the coming weeks and quarters. It’s important to bear in mind that La Rosa only became a public company in Q4/2023, so direct comparisons might not fully reflect the company’s underlying value. However, as it advances, it’s reasonable to anticipate that any gaps in valuation could swiftly close.

Disruptive Ahead Of Its Time

That can actually happen sooner rather than later, resulting from La Rosa showing itself as a disruptive player in a market that is more than evolving; it’s been forced to change. A landmark verdict and $1.8 billion judgment against “Big Real Estate,” including the conglomerate National Association of Realtors (NAR), have sent shockwaves through the industry. Not only because of the size of the award but also because many traditional real estate brokerage houses were left with an antiquated business model. More simply, many competing company commission structures needed to be immediately changed, which certainly can’t happen overnight.

But they have no choice. The lawsuit against NAR and other real estate entities highlighted the long-standing issue of artificially high home sale commissions. This verdict and the staggering judgment sent a clear message about the need for immediate change. It was indeed a massive disruption for the sector. But for La Rosa, who had the vision to see this commission revolution early, it’s a positively transformative event.

In fact, the ruling did more than show the La Rosa CEO as a sector visionary; it put his company in the spotlight for having already implemented a revolutionary commission model and structure that benefits buyers, sellers, and agents alike. Moreover, it exposed them as pioneers in fostering transparency and fairness in real estate transactions. That’s fueling the increase in La Rosa’s growth pace, which has shifted from hyper to warp and shows no signs of slowing.

La Rosa Differences Are Advantages

That’s not surprising. La Rosa Holdings’ differences are advantageous to everyone involved in real estate transactions. They are facilitated through La Rosa encompassing five agent-centric, technology-integrated, cloud-based real estate segments. These allow La Rosa to work beyond traditional residential and commercial brokerage services, evidenced by its ancillary technology-based products and services providing its agents and franchisees with a comprehensive one-stop solution shop to facilitate a transaction from start to close. Better still, the model makes sure commissions go to the right places.

Unlike traditional models that often lead to significant commission splits, La Rosa’s approach ensures that agents retain 100% of their commissions minus a minimal facilitation fee. This model empowers agents financially and aligns with evolving consumer expectations for equitable and efficient real estate services. But La Rosa has pointed to its success being about more than just maximizing profits; it’s about creating a holistic ecosystem where agents thrive through multiple revenue streams and advanced technological tools. It’s an agent-centric approach that is attracting top industry talent.

Expect that to continue, resulting from the tangible impact La Rosa’s innovative model provides its agents. Agents under the La Rosa banner earn substantially more per transaction compared to traditional brokerages. This financial advantage, which rewards agents while creating diversified revenue streams for the company, is a win-win proposition that should continue solidifying La Rosa’s position as a trailblazer in the industry.

A Value Proposition Exposed

Thus, whether comparing La Rosa side by side to billion-dollar market cap companies or appraising them as a stand-alone, the value proposition exposed at its current share price is compelling. Yes, the sector is under pressure from higher interest rates and macro issues. However, that is not slowing La Rosa’s intent to continue acquiring top-performing, significant revenue-generating assets immediately accretive to its operations.

In other words, positioning in a growth company like La Rosa makes the most sense when share prices are low, especially in the face of real-time, fast-growing operational performance. Keep in mind that La Rosa revenues are more than just increasing; they are accruing at a record-setting pace and are expected to reach $100 million by the end of this year. That’s no coincidence, either.

Growth at La Rosa is a testament to proactive adaptation and visionary leadership in an ever-evolving sector. And with La Rosa at the forefront, even an usher, of this industry’s transformative journey, expect an already impressive and steepening growth trajectory to continue.

Disclaimers: This presentation has been created by Hawk Point Media Group, Llc. (HPM) and is responsible for the production and distribution of this content. This presentation should be considered and explicitly regarded as sponsored content. Hawk Point Media Group, LLC. has been compensated to create this content as part of a more extensive digital marketing program by an unrelated third party to the company. Accordingly, this content may be used and syndicated beyond the channels used by Hawk Point Media, Llc. This disclaimer and the link to the broader disclosures must be part of all reproductions. Receiving that referenced compensation creates a conflict of interest because the content presented may only provide a favorable viewpoint of the company featured. The contributors do NOT buy and sell securities in the companies featured. HPM holds ZERO shares and has never owned stock in La Rosa Holdings Corp. The information in this video, article, and related newsletters is not intended to be, nor does it constitute, investment advice or recommendations. Hawk Point Media Group, Llc. strongly urges you to conduct a complete and independent investigation of the respective companies and consider all pertinent risks. Readers are advised to review SEC periodic reports: Forms 10-Q, 10K, Form 8-K, insider reports, Forms 3, 4, 5 Schedule 13D. Never take opinions, articles presented, or content provided as the sole reason to invest in any featured company. Investors must always perform their own due diligence before investing in any publicly traded company and understand the risks involved, including losing their entire investment. For the complete disclosure statement, including compensation received, click HERE.

Media Contact

Company Name: Hawk Point Media

Contact Person: Editorial Dept.

Email: [email protected]

Country: United States

Website: https://hawkpointmedia.com/

){kind=link}